# devtools::install_github("problemofpoints/reservetestr")

library(tidyverse)

library(ChainLadder)

library(reservetestr)

library(broom)

library(broom.mixed)

library(rstanarm)

library(bayesplot)

library(popformatting)

library(patchwork)

# set ggplot2 theme

popformatting::gg_set_theme()

# pull in the subset of the CAS loss reserve database used by Meyers

cas_triangle_db_meyers <- reservetestr::cas_loss_reserve_db %>%

reservetestr::get_meyers_subset()

# extract sample paid loss triangle to use

sample_company <- cas_triangle_db_meyers %>%

dplyr::filter(group_id == 7080 & line == "wkcomp")

paid_triangle <- sample_company %>%

pull(train_tri_set) %>%

.[[1]] %>%

.$paid

paid_triangle_no_exposure <- paid_triangle

attr(paid_triangle_no_exposure, "exposure") <- NULL

paid_triangle

#> dev_lag

#> acc_yr 1 2 3 4 5 6 7 8 9 10

#> 1988 41821 76550 96697 112662 123947 129871 134646 138388 141823 144781

#> 1989 48167 87662 112106 130284 141124 148503 154186 158944 162903 NA

#> 1990 52058 99517 126876 144792 156240 165086 170955 176346 NA NA

#> 1991 57251 106761 133797 154668 168972 179524 187266 NA NA NA

#> 1992 59213 113342 142908 165392 179506 189506 NA NA NA NA

#> 1993 59475 111551 138387 160719 175475 NA NA NA NA NA

#> 1994 65607 110255 137317 159972 NA NA NA NA NA NA

#> 1995 56748 96063 122811 NA NA NA NA NA NA NA

#> 1996 52212 92242 NA NA NA NA NA NA NA NA

#> 1997 43962 NA NA NA NA NA NA NA NA NA

#> attr(,"exposure")

#> [1] 195712 212194 219796 249595 268293 316726 344287 356880 313412 261261Bayesian Chain Ladder

Use Bayesian methods to replicate the Chain Ladder reserving method

Goal

The goal of this post is to use the rstanarm package to run a Bayesian Chain Ladder reserving method on the CAS Loss Reserve Database. The cross classified generalized linear model (GLM) formulation of the Chain Ladder will be used.

See STOCHASTIC LOSS RESERVING USING GENERALIZED LINEAR MODELS for a description of the cross classified GLM formulation. The same example triangle used in the monograph is also used in this post.

In future posts, we will investigate the results further and explore extensions to the baseline model.

Data

Standard chain ladder estimate

We can use the glmReserve function from the ChainLadder package to produce the standard Chain Ladder reserve estimate. This method provides both a point estimate and a distribution of estimates, using a bootstrapping approach. This function uses the cross classified over-dispersed Poisson GLM formulation applied to an incremental paid loss triangle, which exactly re-produces the traditional Chain Ladder reserve estimate. For convenience in producing the Bayesian equivalent, we use the Negative Binomial distribution instead of the over-dispersed Poisson. This is done by setting the nb parameter to TRUE in glmReserve. We still achieve mean results essentially equivalent to the traditional chain ladder estimate.

est_chainladder_nb <- glmReserve(paid_triangle_no_exposure,

var.power = 1, link.power = 0, cum = TRUE,

mse.method = "bootstrap", nsim = 5000,

nb = TRUE)

est_chainladder_nb$summary %>%

rownames_to_column("Acc Yr") %>%

mutate_at(c(2,4:6), popformatting::number_format) %>%

flextable::regulartable() %>%

popformatting::ft_theme(add_w = 0.0, add_h = 0.00, add_h_header = 0.00) %>%

flextable::bg(i = nrow(est_chainladder_nb$summary),

bg = "#F2F2F2", part = "body") %>%

popformatting::add_title_header("Chain ladder reserve estimate",

font_size = 18) %>%

flextable::fontsize(size = 16, part = "all")Chain ladder reserve estimate |

||||||

Acc Yr |

Latest |

Dev.To.Date |

Ultimate |

IBNR |

S.E |

CV |

1989 |

162,903 |

0.9794376 |

166,323 |

3,420 |

333 |

0.09749463 |

1990 |

176,346 |

0.9559292 |

184,476 |

8,130 |

542 |

0.06664080 |

1991 |

187,266 |

0.9255245 |

202,335 |

15,069 |

823 |

0.05462254 |

1992 |

189,506 |

0.8931800 |

212,170 |

22,664 |

1,126 |

0.04966852 |

1993 |

175,475 |

0.8464949 |

207,296 |

31,821 |

1,480 |

0.04651688 |

1994 |

159,972 |

0.7788088 |

205,406 |

45,434 |

2,164 |

0.04763981 |

1995 |

122,811 |

0.6710177 |

183,022 |

60,211 |

3,047 |

0.05060250 |

1996 |

92,242 |

0.5329782 |

173,069 |

80,827 |

4,705 |

0.05820747 |

1997 |

43,962 |

0.2934360 |

149,818 |

105,856 |

8,211 |

0.07756789 |

total |

1,310,483 |

0.7782358 |

1,683,915 |

373,432 |

11,626 |

0.03113416 |

The total Chain Ladder reserve estimate for this triangle is 373,432 with an overall coefficient of variation (CV) of 3.11%.

We can also output the underlying GLM formula and fitted parameters.

summary(est_chainladder_nb, type = "model")

#>

#> Call:

#> glm.nb(formula = value ~ factor(origin) + factor(dev), data = ldaFit,

#> init.theta = 331.5546543, link = log)

#>

#> Deviance Residuals:

#> Min 1Q Median 3Q Max

#> -2.0547 -0.8338 0.0000 0.7548 2.4347

#>

#> Coefficients:

#> Estimate Std. Error z value Pr(>|z|)

#> (Intercept) 10.64796 0.02678 397.680 < 2e-16 ***

#> factor(origin)1989 0.14524 0.02639 5.503 3.73e-08 ***

#> factor(origin)1990 0.24120 0.02752 8.765 < 2e-16 ***

#> factor(origin)1991 0.36897 0.02875 12.832 < 2e-16 ***

#> factor(origin)1992 0.39068 0.03025 12.913 < 2e-16 ***

#> factor(origin)1993 0.36907 0.03218 11.471 < 2e-16 ***

#> factor(origin)1994 0.35424 0.03480 10.180 < 2e-16 ***

#> factor(origin)1995 0.24495 0.03873 6.325 2.53e-10 ***

#> factor(origin)1996 0.18578 0.04547 4.086 4.39e-05 ***

#> factor(origin)1997 0.04312 0.06128 0.704 0.482

#> factor(dev)2 -0.20610 0.02598 -7.934 2.13e-15 ***

#> factor(dev)3 -0.74477 0.02721 -27.376 < 2e-16 ***

#> factor(dev)4 -1.01574 0.02854 -35.591 < 2e-16 ***

#> factor(dev)5 -1.44957 0.03017 -48.041 < 2e-16 ***

#> factor(dev)6 -1.84320 0.03228 -57.094 < 2e-16 ***

#> factor(dev)7 -2.14799 0.03517 -61.072 < 2e-16 ***

#> factor(dev)8 -2.34589 0.03944 -59.476 < 2e-16 ***

#> factor(dev)9 -2.50783 0.04676 -53.636 < 2e-16 ***

#> factor(dev)10 -2.65570 0.06380 -41.622 < 2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> (Dispersion parameter for Negative Binomial(331.5547) family taken to be 1)

#>

#> Null deviance: 11754.138 on 54 degrees of freedom

#> Residual deviance: 54.947 on 36 degrees of freedom

#> AIC: 962.24

#>

#> Number of Fisher Scoring iterations: 1

#>

#>

#> Theta: 331.6

#> Std. Err.: 64.7

#>

#> 2 x log-likelihood: -922.243The factor(origin) parameters, often also known as alpha parameters, represent the accident year level of loss. The factor(dev) parameters (or beta parameters) represent the development year direction. We can re-arrange the fitted development year parameters to re-create the standard chain ladder link ratios, as shown in the table below.

model_params <- broom::tidy(est_chainladder_nb$model) %>%

separate(term, into = c("factor","variable","value"), "\\(|\\)") %>%

mutate(value = as.numeric(value)) %>%

mutate(value = case_when(variable == "Intercept" ~ 1,

variable == "origin" ~ value - 1988 + 1,

variable == "dev" ~ value)) %>%

mutate(variable = case_when(variable == "Intercept" ~ "origin",

TRUE ~ variable)) %>%

select(variable, value, estimate) %>%

bind_rows(tibble(variable = "dev",value=1,estimate=0)) %>%

mutate(estimate2 = case_when(variable == "origin" & value == 1 ~ estimate[1],

variable == "origin" & value != 1 ~ estimate[1]+estimate,

variable == "dev" ~ estimate)) %>%

mutate(estimate3 = case_when(variable == "origin" ~ exp(estimate2),

variable == "dev" ~ exp(estimate))) %>%

mutate(estimate_normalized = case_when(variable == "origin" ~

exp(estimate2) * sum(.$estimate3[.$variable=="dev"]),

variable == "dev" ~

estimate3 / sum(.$estimate3[.$variable=="dev"]))) %>%

arrange(variable, value)

model_params_link <- model_params %>%

filter(variable == "dev") %>%

mutate(link = lead(cumsum(estimate3) / lag(cumsum(estimate3))))

model_params_link %>%

select(`Dev period` = value, `LN(Betas)` = estimate, Betas = estimate3,

Normalized = estimate_normalized, `Link ratios` = link) %>%

mutate_at(2:5, number_format, digits = 3) %>%

flextable::regulartable() %>%

ft_theme() %>%

add_title_header("GLM parameters - development factors", font_size = 18) %>%

flextable::fontsize(size = 16, part = "all")GLM parameters - development factors |

||||

Dev period |

LN(Betas) |

Betas |

Normalized |

Link ratios |

1 |

0.000 |

1.000 |

0.293 |

1.814 |

2 |

-0.206 |

0.814 |

0.239 |

1.262 |

3 |

-0.745 |

0.475 |

0.139 |

1.158 |

4 |

-1.016 |

0.362 |

0.106 |

1.089 |

5 |

-1.450 |

0.235 |

0.069 |

1.055 |

6 |

-1.843 |

0.158 |

0.046 |

1.038 |

7 |

-2.148 |

0.117 |

0.034 |

1.030 |

8 |

-2.346 |

0.096 |

0.028 |

1.025 |

9 |

-2.508 |

0.081 |

0.024 |

1.021 |

10 |

-2.656 |

0.070 |

0.021 |

NA |

Residual diagnostics of standard chain ladder

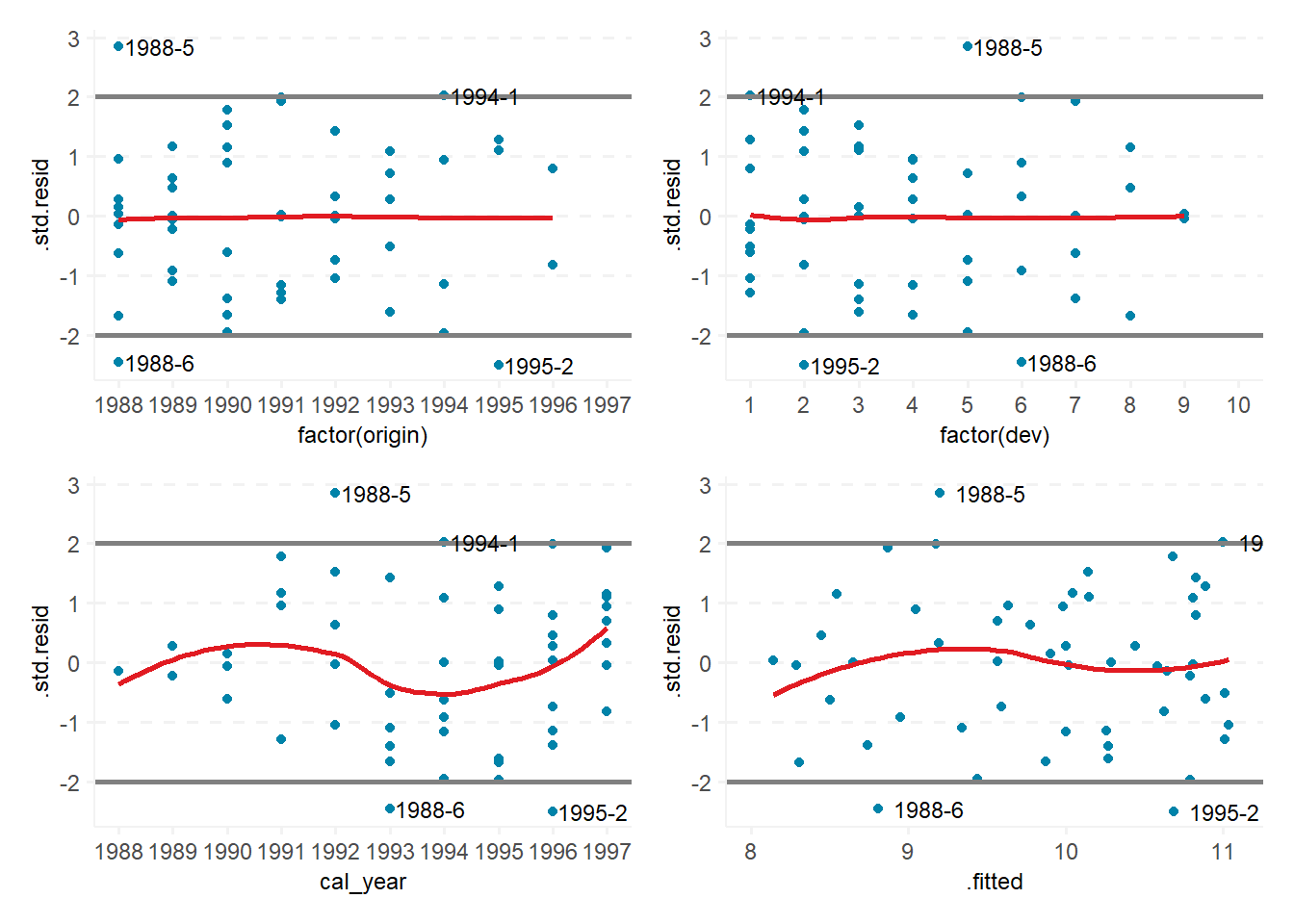

Given we’ve used the GLM formulation to produce the Chain Ladder estimate, we can look at residual plots to understand the goodness-of-fit of our model.

residuals_cl <- broom::augment(est_chainladder_nb$model) %>%

mutate_at(3:4, ~ as.integer(paste(.x))) %>%

mutate(cal_year = `factor(origin)` + `factor(dev)` - 1)

residual_plot <- function(resid_df, y_var, x_var, x_breaks = TRUE){

x_var_en <- rlang::enquo(x_var)

y_var_en <- rlang::enquo(y_var)

outliers <- resid_df %>%

filter(abs(!!y_var_en) > 2)

ggplot(data = resid_df, aes(y = !!y_var_en, x = !!x_var_en)) +

geom_point() +

geom_smooth(se = FALSE) +

geom_hline(yintercept = c(-2,2)) +

geom_text(aes(x = !!x_var_en, y = !!y_var_en, label = .rownames),

data = outliers, hjust = 0, size = 3, nudge_x = 0.1) +

theme(axis.title = element_text(size = 9), axis.text = element_text(size = 9)) +

if(x_breaks){

scale_x_continuous(breaks = resid_df %>% select(!!x_var_en) %>%

distinct() %>% pull())

}

}

gg_origin <- residual_plot(residuals_cl, .std.resid, `factor(origin)`)

gg_dev <- residual_plot(residuals_cl, .std.resid, `factor(dev)`)

gg_cal <- residual_plot(residuals_cl, .std.resid, cal_year)

gg_fit <- residual_plot(residuals_cl, .std.resid, .fitted, FALSE)

gg_origin + gg_dev +

gg_cal + gg_fit +

plot_layout(ncol = 2)

These plots show the standardized residuals versus accident (origin) year, development period, calendar year, and fitted values. All of the plots look reasonable with the residuals randomly centered around zero and only a few outliers in each.

Bayesian chain ladder using rstanarm

Now we can take the same GLM formulation, but use Bayesian methods for the estimation. The rstanarm package makes it very straightforward to do this.

First we convert our triangle object to “long” form.

long_paid_tri <- cum2incr(paid_triangle) %>%

as.data.frame(paid_triangle) %>%

filter(!is.na(value))

head(long_paid_tri)

#> acc_yr dev_lag value

#> 1 1988 1 41821

#> 2 1989 1 48167

#> 3 1990 1 52058

#> 4 1991 1 57251

#> 5 1992 1 59213

#> 6 1993 1 59475Then we can call the stan_glm function to fit our model.

nb_theta <- est_chainladder_nb$model$theta

est_cl_bayesian_nb <- stan_glm(value ~ factor(acc_yr) + factor(dev_lag),

family = neg_binomial_2(link = "log"),

prior_aux = normal(0, nb_theta * 2),

data = long_paid_tri)broom.mixed::tidy(est_cl_bayesian_nb, intervals = TRUE, prob = 0.95) %>%

mutate_at(2:3, popformatting::number_format, digits = 3) %>%

flextable::regulartable() %>%

popformatting::ft_theme() %>%

flextable::align(j=1, align="left", part = "all") %>%

add_title_header("Bayesian chain ladder parameter summary",

font_size = 18) %>%

flextable::fontsize(size = 16, part = "all")Bayesian chain ladder parameter summary |

||

term |

estimate |

std.error |

(Intercept) |

10.648 |

0.034 |

factor(acc_yr)1989 |

0.146 |

0.032 |

factor(acc_yr)1990 |

0.242 |

0.034 |

factor(acc_yr)1991 |

0.370 |

0.036 |

factor(acc_yr)1992 |

0.392 |

0.037 |

factor(acc_yr)1993 |

0.370 |

0.040 |

factor(acc_yr)1994 |

0.356 |

0.043 |

factor(acc_yr)1995 |

0.247 |

0.048 |

factor(acc_yr)1996 |

0.189 |

0.057 |

factor(acc_yr)1997 |

0.045 |

0.076 |

factor(dev_lag)2 |

-0.206 |

0.031 |

factor(dev_lag)3 |

-0.745 |

0.032 |

factor(dev_lag)4 |

-1.016 |

0.035 |

factor(dev_lag)5 |

-1.450 |

0.038 |

factor(dev_lag)6 |

-1.843 |

0.039 |

factor(dev_lag)7 |

-2.147 |

0.044 |

factor(dev_lag)8 |

-2.344 |

0.046 |

factor(dev_lag)9 |

-2.507 |

0.054 |

factor(dev_lag)10 |

-2.654 |

0.077 |

We can compare the parameter estimates from our two methods and see that they are in close agreement.

broom.mixed::tidy(est_cl_bayesian_nb, intervals = FALSE) %>%

bind_cols(broom::tidy(est_chainladder_nb$model) %>% select(-term, "Standard"=estimate)) %>%

select(term, Bayesian = estimate, Standard) %>%

mutate(`% error` = Bayesian / Standard - 1) %>%

mutate_at(2:3, number_format, digits = 3) %>%

mutate_at(4, pct_format) %>%

flextable::regulartable() %>%

popformatting::ft_theme() %>%

flextable::align(j=1, align="left", part = "all") %>%

add_title_header("Parameter estimate comparison", font_size = 18) %>%

flextable::fontsize(size = 16, part = "all")Parameter estimate comparison |

|||

term |

Bayesian |

Standard |

% error |

(Intercept) |

10.648 |

10.648 |

-0.00% |

factor(acc_yr)1989 |

0.146 |

0.145 |

0.82% |

factor(acc_yr)1990 |

0.242 |

0.241 |

0.37% |

factor(acc_yr)1991 |

0.370 |

0.369 |

0.41% |

factor(acc_yr)1992 |

0.392 |

0.391 |

0.28% |

factor(acc_yr)1993 |

0.370 |

0.369 |

0.27% |

factor(acc_yr)1994 |

0.356 |

0.354 |

0.44% |

factor(acc_yr)1995 |

0.247 |

0.245 |

0.88% |

factor(acc_yr)1996 |

0.189 |

0.186 |

1.66% |

factor(acc_yr)1997 |

0.045 |

0.043 |

5.24% |

factor(dev_lag)2 |

-0.206 |

-0.206 |

0.06% |

factor(dev_lag)3 |

-0.745 |

-0.745 |

0.06% |

factor(dev_lag)4 |

-1.016 |

-1.016 |

0.07% |

factor(dev_lag)5 |

-1.450 |

-1.450 |

0.04% |

factor(dev_lag)6 |

-1.843 |

-1.843 |

-0.03% |

factor(dev_lag)7 |

-2.147 |

-2.148 |

-0.07% |

factor(dev_lag)8 |

-2.344 |

-2.346 |

-0.08% |

factor(dev_lag)9 |

-2.507 |

-2.508 |

-0.05% |

factor(dev_lag)10 |

-2.654 |

-2.656 |

-0.06% |

We can also confirm that the reserve estimates produced by both methods are the same.

future_tri <- cum2incr(paid_triangle) %>%

as.data.frame(paid_triangle) %>%

filter(is.na(value)) %>%

mutate(acc_yr = factor(acc_yr), dev_lag = factor(dev_lag)) %>%

select(-value)post_predict_draws <- future_tri %>%

tidybayes::add_predicted_draws(est_cl_bayesian_nb) %>%

mutate_at(7, as.double)

bayesian_cl_summary <- post_predict_draws %>%

group_by(acc_yr, .draw) %>%

summarise(.prediction = sum(.prediction)) %>%

summarise(mean_est = mean(.prediction), sd_est = sd(.prediction),

cv = sd(.prediction) / mean(.prediction))

sim_total <- post_predict_draws %>%

group_by(.draw) %>%

summarise(.prediction = sum(.prediction))

bayesian_cl_summary <- bayesian_cl_summary %>%

bind_rows(tibble(acc_yr = "total",

mean_est = mean(sim_total$.prediction),

sd_est = sd(sim_total$.prediction),

cv = sd(sim_total$.prediction)/mean(sim_total$.prediction))) %>%

mutate(Latest = est_chainladder_nb$summary$Latest, IBNR = mean_est,

`S.E.` = sd_est, CV = cv,

Ultimate = est_chainladder_nb$summary$Latest + mean_est,

`Dev.To.Date` = Latest / Ultimate)

bayesian_cl_summary %>%

select(`Acc Yr` = acc_yr, Latest, `Dev.To.Date`, Ultimate, IBNR, `S.E.`, CV) %>%

mutate_at(c(2,4:6), number_format) %>%

flextable::regulartable() %>%

popformatting::ft_theme(add_w = 0.0, add_h = 0.00, add_h_header = 0.00) %>%

flextable::bg(i = nrow(est_chainladder_nb$summary), bg = "#F2F2F2", part = "body") %>%

popformatting::add_title_header("Bayesian chain ladder reserve estimate", font_size = 18) %>%

flextable::fontsize(size = 16, part = "all")Bayesian chain ladder reserve estimate |

||||||

Acc Yr |

Latest |

Dev.To.Date |

Ultimate |

IBNR |

S.E. |

CV |

1989 |

162,903 |

0.9793075 |

166,345 |

3,442 |

352 |

0.10232483 |

1990 |

176,346 |

0.9556824 |

184,524 |

8,178 |

591 |

0.07232153 |

1991 |

187,266 |

0.9252061 |

202,405 |

15,139 |

896 |

0.05916681 |

1992 |

189,506 |

0.8927995 |

212,260 |

22,754 |

1,207 |

0.05303895 |

1993 |

175,475 |

0.8460864 |

207,396 |

31,921 |

1,630 |

0.05107670 |

1994 |

159,972 |

0.7780818 |

205,598 |

45,626 |

2,310 |

0.05062487 |

1995 |

122,811 |

0.6700935 |

183,274 |

60,463 |

3,271 |

0.05410145 |

1996 |

92,242 |

0.5319070 |

173,418 |

81,176 |

5,144 |

0.06337166 |

1997 |

43,962 |

0.2923913 |

150,353 |

106,391 |

8,431 |

0.07924123 |

total |

1,310,483 |

0.7774703 |

1,685,573 |

375,090 |

12,163 |

0.03242720 |

The 375,090 estimate from the Bayesian method is only 0.44% different than the traditional estimate. Similarly, the total CV of 3.24% is close to the traditional estimate of 3.11%.

Bayesian posterior predictive checks

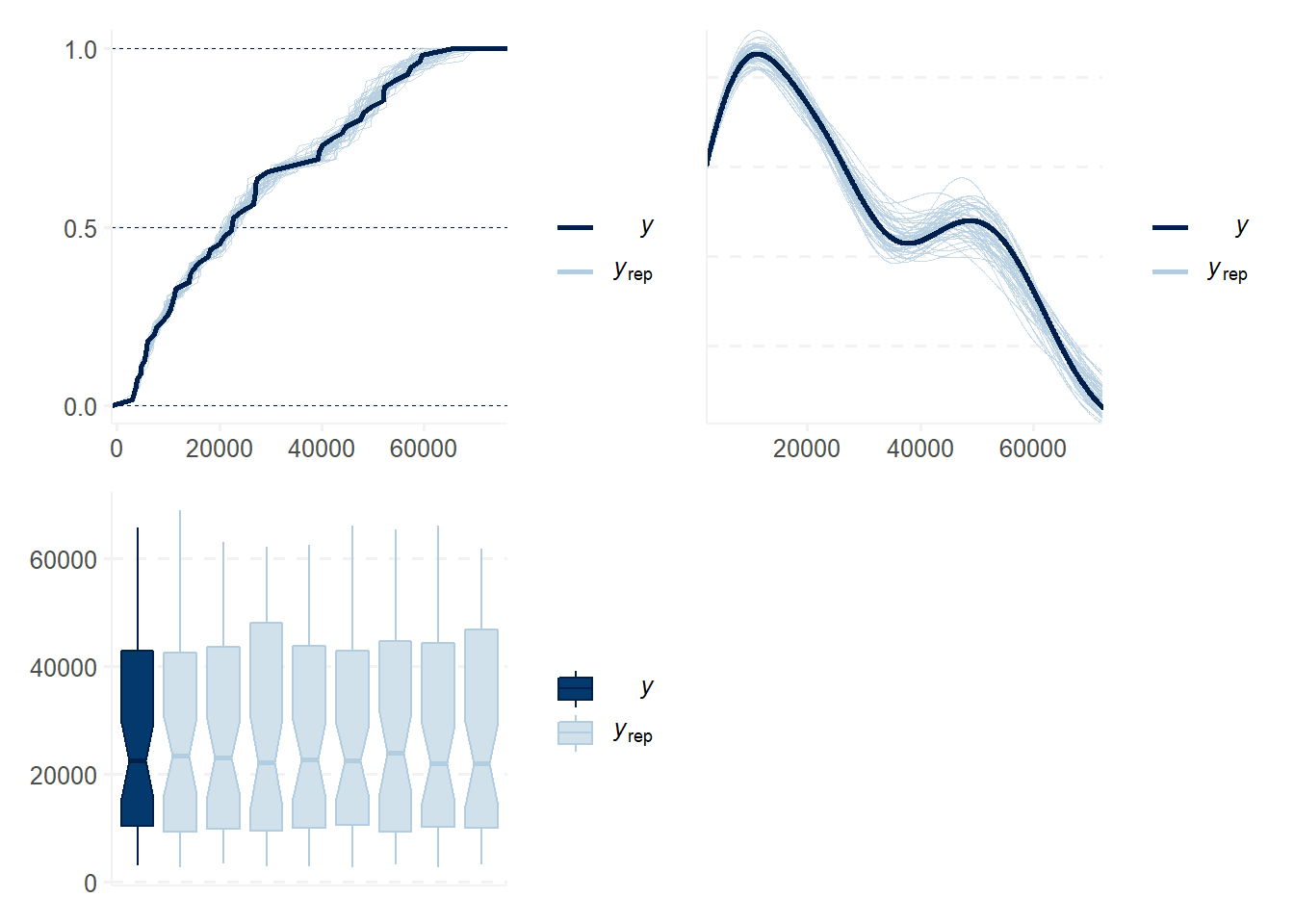

Using a Bayesian framework allows us to more fully interrogate our model and the assumptions underlying it. We can look at the distribution of parameters and predictions, making valid probabilistic statements about our results.

pp_check(est_cl_bayesian_nb, "ecdf_overlay") +

pp_check(est_cl_bayesian_nb, "dens_overlay") +

pp_check(est_cl_bayesian_nb, "boxplot") +

plot_layout(ncol = 2)

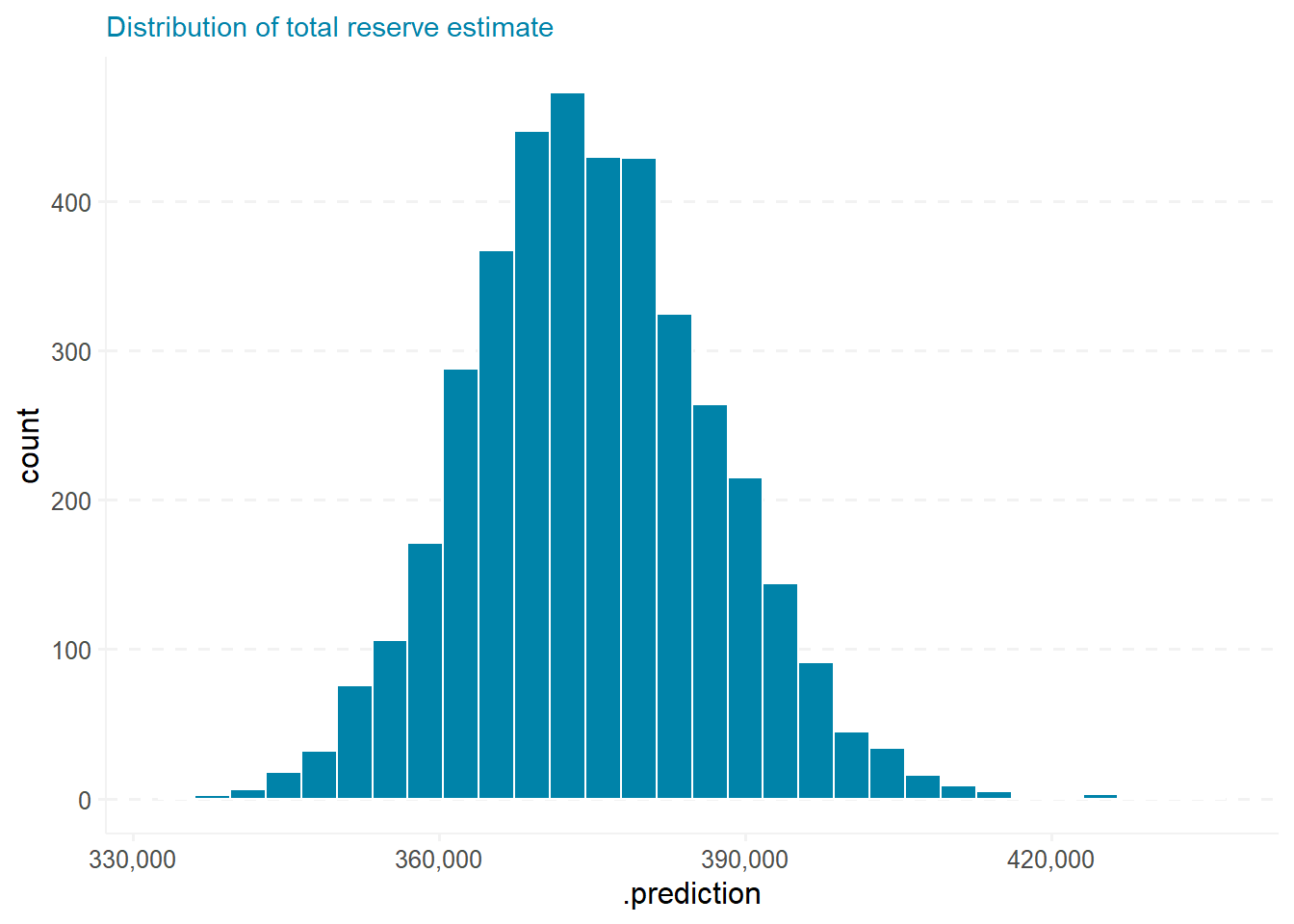

Below is a histogram of the total estimated reserves.

sim_total %>%

ggplot(aes(x = .prediction)) +

geom_histogram() +

scale_x_continuous(labels = number_format) +

ggtitle("Distribution of total reserve estimate")

Further enhancements

Now that we have successfully replicated the standard chain ladder method using Bayesian methods, we can move forward taking advantage of the flexibility that the Bayesian framework provides.

For example, we can:

- Add informative prior distributions on the parameters

- Back-test reserve estimates to determine accuracy in forecasting reserves

- Test other distribution families (e.g. Gamma, Skew Normal, etc.)

- Add additional variables, such as a calendar year effect